This, in turn, gives businesses a clear picture of where they stand. This trial balance type allows businesses have a summarized view of all the account balances post-adjustment to respective expenditures. The second method is simple and fast but is considered less systematic. This method is usually used by small companies where only a few adjusting entries are found at the end of the accounting period.

Related AccountingTools Courses

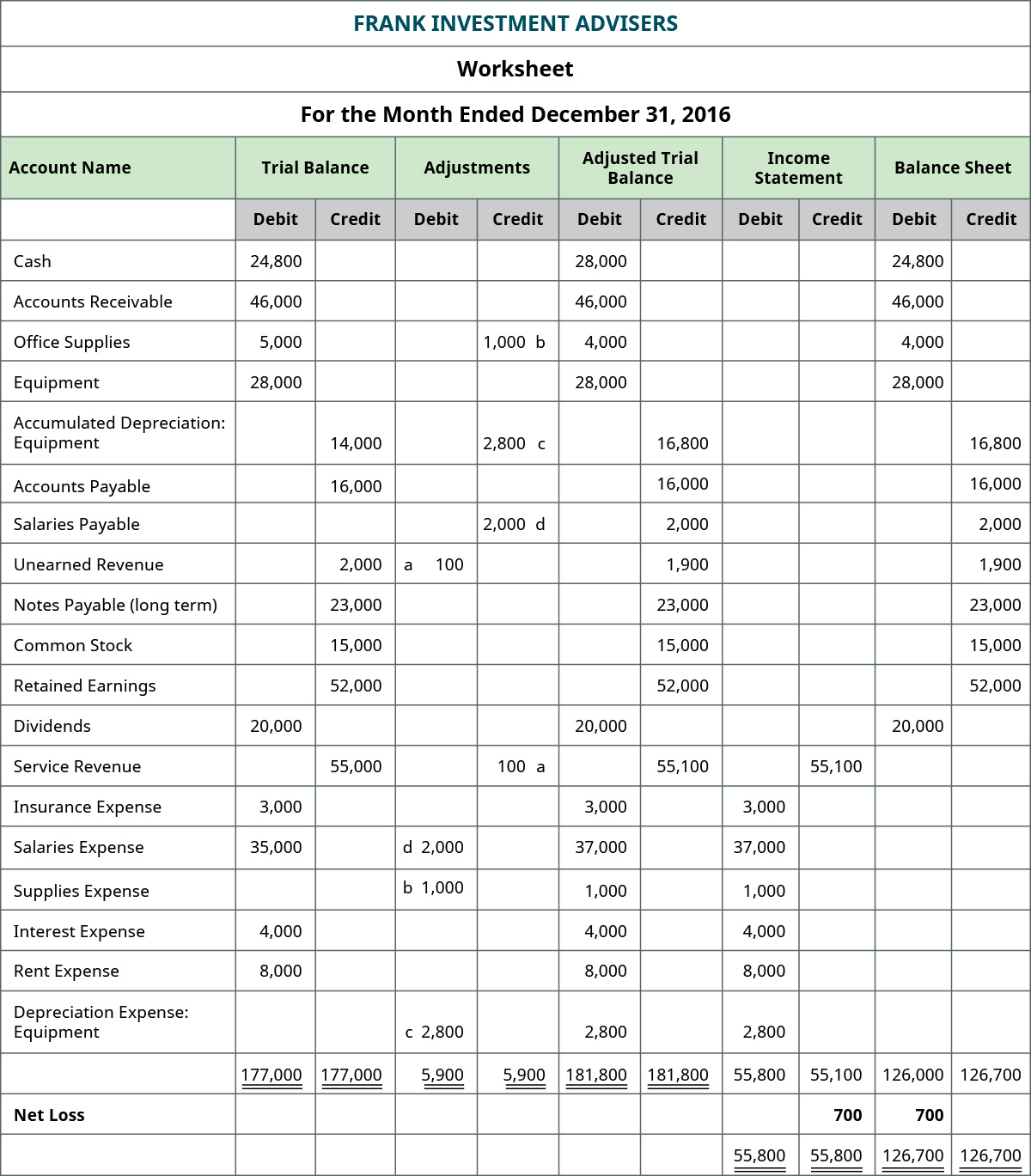

As with the unadjusted trial balance, transferring informationfrom T-accounts to the adjusted trial balance requiresconsideration of the final balance in each account. If the finalbalance in the ledger account (T-account) is a debit balance, youwill record the total in the left column of the trial balance. Ifthe final balance in the ledger account (T-account) is a creditbalance, you will record the total in the right column. We are using the same posting accounts as we did for the unadjusted trial balance just adding on. Notice how we start with the unadjusted trial balance in each account and add any debits on the left and any credits on the right. Adjusted trial balance records the account balances of an organization after adjusting the transaction to various expenses, including the depreciation amount, accrued expenses, payroll expenses, etc.

Unadjusted Trial Balance

Such expenses might include paying for a rented space or any upcoming payments in the queue. Most accounting software will let you generate a trial balance at any point in time to allow you to assess the current state of your accounts. Accrued revenues are revenues earned, but not received in monetary terms, and therefore represent receivables. Hence, the trial balance includes all considerable adjustments, which is termed as adjustment trial balance.

Preparing the Financial Statements

Adjusted trial balances are prepared at the end of the accounting cycle and are used to help prepare the financial statements for the period. Before the adjusted TB can be prepared, the year-end adjustments must be made. These adjustments usually include adjustments for prepaid and accrued expenses along with non-cash expenses like depreciation. These adjustments are added to the unadjusted trial balance on the accounting worksheet and the new adjusted TB is prepared.

After we post the adjusting entries, it is necessary to check our work and prepare an adjusted trial balance. This initial trial balance includes all the ledger balances before any adjustments are made. List each account cost reconciliation in construction projects and its balance, and ensure that the total debits equal total credits. Adjusted Trial Balance refers to the general ledger balances reflecting adjustments, which include accrued expenditure and non-cash expenses.

- Deferred revenue is “earned” upon delivery of goods or services to customers.

- As with all financial reports, trial balances are always prepared with a heading.

- Financial statements drawn on the basis of this version of trial balance generally comply with major accounting frameworks, like GAAP and IFRS.

- An adjusted trial balance is a listing of all company accounts that will appear on the financial statements after year-end adjusting journal entries have been made.

The format of an adjusted trial balance is same as that of unadjusted trial balance. For example, if a company has earned interest income that hasn’t been recorded, you would make an adjusting entry to recognize this income. After incorporating the adjustments above, the adjusted trial balance would look like this. After incorporating the $900 credit adjustment, the balance will now be $600 (debit). This article is not intended to provide tax, legal, or investment advice, and BooksTime does not provide any services in these areas.

It is just for the purpose of explanation, and you don’t need to change the color of account titles in your homework assignments or examination questions. Note that only active accounts that will appear on the financial statements must to be listed on the trial balance. If an account has a zero balance, there is no need to list it on the trial balance.

The next step in the accounting cycle would be to complete the financial statements. Adjusted trial balance is a list of all the accounts of a business with their adjusted balances. A trial balance only contains ending balances of your accounting accounts, while the general ledger has detailed transactions of the accounts. The next type of adjustment is the accrual, which ensures inclusion of the future payments that the business entity is entitled to make.

As with all financial reports, trial balances are always prepared with a heading. Typically, the heading consists of three lines containing the company name, name of the trial balance, and date of the reporting period. Preparing an adjusted trial balance is the fifth step in the accounting cycle and is the last step before financial statements can be produced. Note that while a trial balance is helpful in the double-entry system as an initial check of account balances, it won’t catch every accounting error. Each account with a balance in your accounting system, such as accounts receivable and accounts payable, appears in the trial balance with its respective balance–debits on the left and credits on the right.

If they aren’t equal, the trial balance was prepared incorrectly or the journal entries weren’t transferred to the ledger accounts accurately. In a manual accounting system, an unadjusted trial balance might be prepared by a bookkeeper to be certain that the general ledger has debit amounts equal to the credit amounts. After that is the case, the unadjusted trial balance is used by an accountant to indicate the necessary adjusting entries and the resulting adjusted balances.